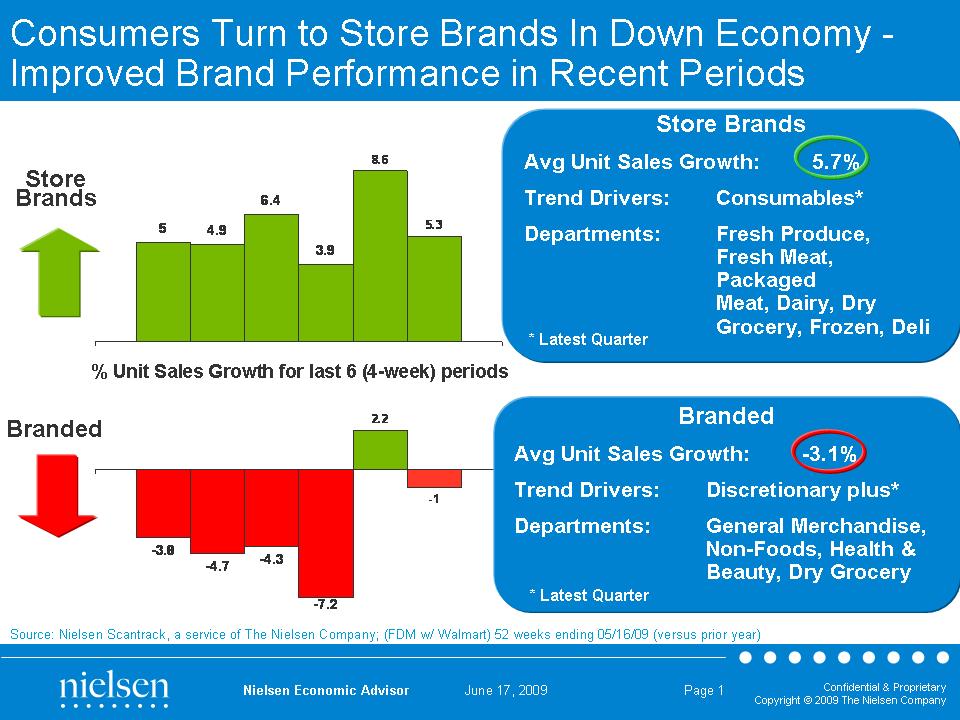

Consumers Continue Turn To Store Brands, But Brands Showing Improvement

Over the latest six (4-week) periods ending 5/16/2009, store brand unit sales averaged a 5.7% increase in consumer-packaged-goods departments tracked by Nielsen in food, drug and mass-merchandisers (including Walmart). Most of this growth is from edible departments (i.e., fresh meat, fresh produce, packaged meat, dairy, dry grocery, frozen and deli). While branded unit sales declined, on average by 3.1%, unit sales in the last two periods were up 2.2% and off 1%, respectively. While this is not a definitive sign that brands are turning the tide in our down economy, it is definitely a positive sign for brand marketers. Departments contributing to the largest declines in branded unit sales are mostly non-edibles (i.e., health & beauty, non-food and general merchandise), but the dry grocery department is having growth challenges too.

For the latest annual period, store brand unit sales reach a 21.3% share and we see share gains in all departments. However, this means that branded products still drive the vast majority (79%) of unit sales. Store brand unit shares range from a high of 40% in the dairy department to a low of 1% in alcoholic beverages.

As we look at the last quarter within the latest annual period, we see unit growth improvements for both store brands and branded departments, but branded sales are negative in most departments. But the fact that branded unit sales trends are improving is a sign that manufacturer actions in the areas of new products, promotions and advertising are impacting consumer purchase decisions.

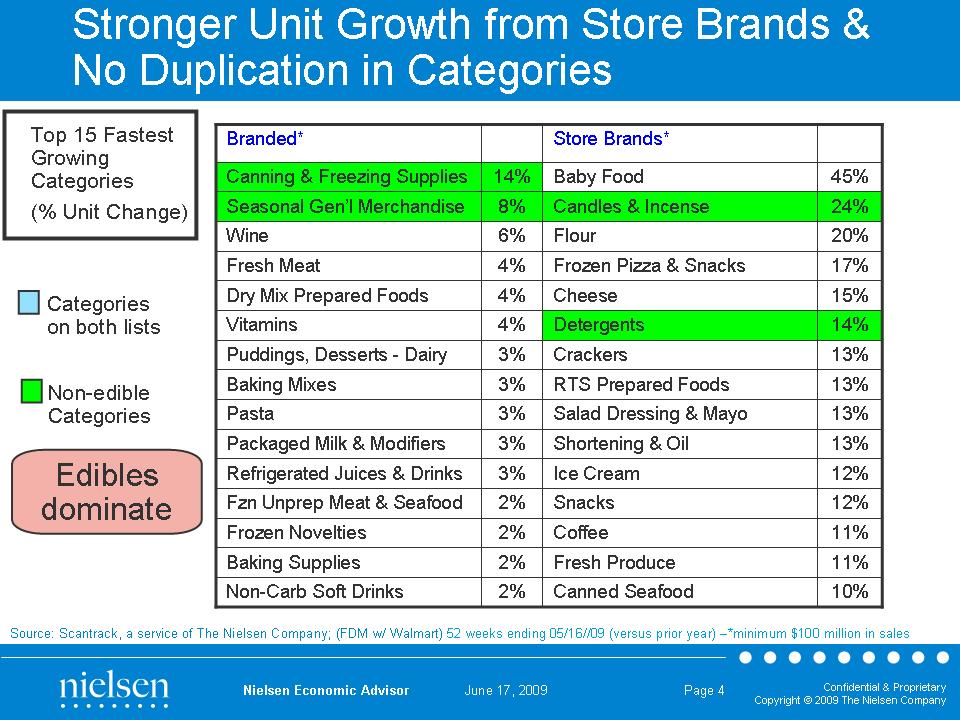

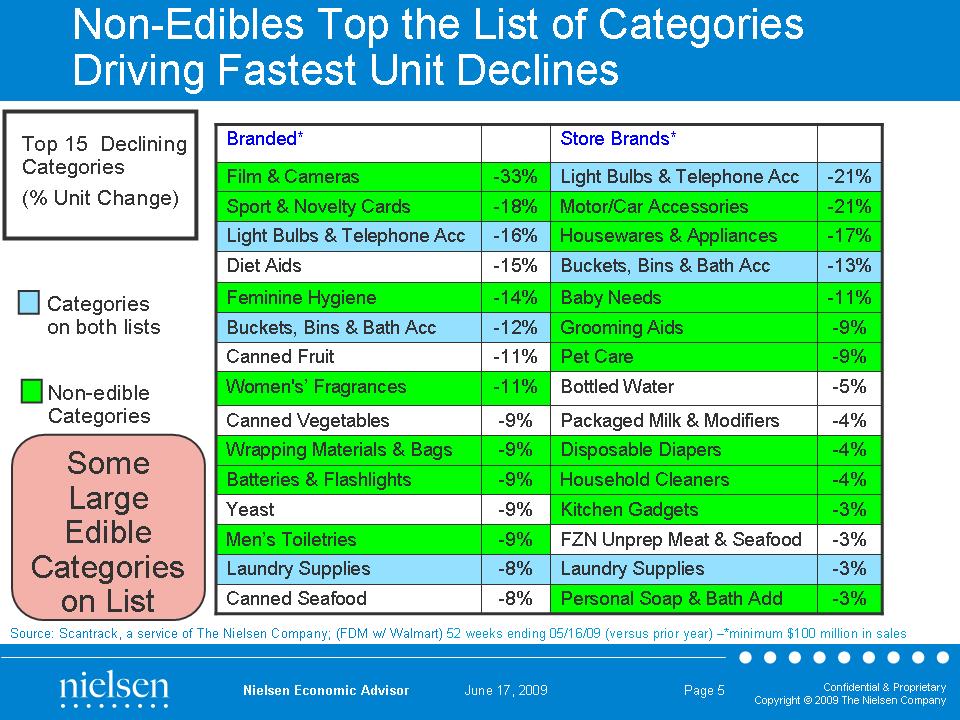

It is also interesting to see how the categories driving the greatest unit brand growth are food and beverage categories, the same pattern as noted for store brands. The categories struggling the most are mostly discretionary categories.

Successful manufacturers will be those who dig deeper into these data and collaborate with their retail partners to drive both brand and store brand sales which yield stronger overall category sales.

Source: Nielsen Wire

For the latest annual period, store brand unit sales reach a 21.3% share and we see share gains in all departments. However, this means that branded products still drive the vast majority (79%) of unit sales. Store brand unit shares range from a high of 40% in the dairy department to a low of 1% in alcoholic beverages.

As we look at the last quarter within the latest annual period, we see unit growth improvements for both store brands and branded departments, but branded sales are negative in most departments. But the fact that branded unit sales trends are improving is a sign that manufacturer actions in the areas of new products, promotions and advertising are impacting consumer purchase decisions.

It is also interesting to see how the categories driving the greatest unit brand growth are food and beverage categories, the same pattern as noted for store brands. The categories struggling the most are mostly discretionary categories.

Successful manufacturers will be those who dig deeper into these data and collaborate with their retail partners to drive both brand and store brand sales which yield stronger overall category sales.

Source: Nielsen Wire