So Why Even Bother Shopping at a Grocery Store?

Back in October, I saw a few jaws drop during a session at the inaugural Groceryshop conference, when a presenter questioned the need for physical stores.

The speaker was Pradeep Elankumaran, co-founder and CEO of San Mateo, Calif.-based pure-play digital grocer Farmstead.

I thought the question was particularly timely. I mean, most surveys seem to indicate that, while consumers are increasingly embracing online grocery shopping, they also express a desire and affection for the experience delivered by a trip to the store.

So I reached out to Elankumaran to elaborate.

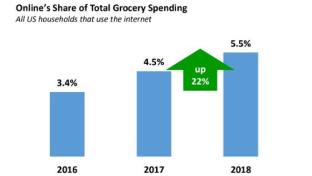

“Grocery stores make up about 92 percent of the $800 billion U.S. grocery space, with online groceries making up the other 8 percent, so they are not going away tomorrow,” he acknowledged via email. “However, it’s also very true that the act of grocery shopping – driving to a supermarket, picking out good produce, walking all over the rest of the store, then waiting in line and then driving back home – is not very relevant or necessary in 2018, or 2019 for that matter. We get everything besides perishables delivered to our doorstep, and there are companies like Farmstead making perishables dropped off at your doorstep cost only as much as what you normally pay at the store, with no delivery fees.”

Elankumaran pointed out that supermarkets and their distribution centers have expensive cost structures – costs that retailers, of course, have perennially striven to drive down. “Add food waste to the mix, along with high-turnover store workers, and you have low-margin businesses,” he said.

“The crux of the problem here,” Elankumaran continued, “is that stores have a ton of forward-deployed inventory sitting inside, and picking for ecommerce inside just cannot support the customer experience that’s required to turn that 8 percent adoption of buying groceries online to 92 percent. We need a new ecommerce-centric operating model. While the stores won’t disappear next year, they inevitably will be smaller and more focused on ecommerce and delivery, more akin to a warehouse than a standard customer-focused store. Click-and-collect is a temporary state – when delivery is free, why go to the store?”

As someone who enjoys going to the grocery store (and I think there’s a few of us left), I’d argue that for true lovers of food – those who embrace the eating experience as one of life’s pleasures and don’t just view calories as fuel – the experience of seeing, smelling, touching and tasting trumps the cold, drab process of mouse-clicking weekly rations to one’s door. And as retailers are working on last-mile solutions and seamless experiences across all platforms, they’re also investing in the savory tangibles of the physical store.

But I recognize that change is not only coming, it’s spewing forth from a fire hose.

Elankumaran’s near-future predictions include:

- Online grocery will grow from 8 percent to roughly 20 percent as consumers get a lot less anxious about buying produce online.

- Grocers will try to move to pure ecommerce models to handle the rapid growth, and will be stymied by existing unionized labor requirements.

- Grocers will scale out their private label on any channel they can get their hands on.

- Indoor farms will become increasingly prominent, putting out higher quality at lower cost for a year-round supply of fresh produce.

- On-demand freshly prepared meals delivered in under 30 minutes will see aggressive growth.

“The innovator’s dilemma is currently real for every grocer on the planet, many of whom don’t understand the nuances of technology-driven marketing,” Elankumaran said. “Not many existing supermarkets are prepared for the impact, even though they are doing their best to adopt as much tech as they can. Unfortunately, we’ve found that margin improvements required to win online groceries mean that they will probably have to be technology companies, applying data and code to stitch together a new way to build for the next hundreds of millions who have really started to dislike shopping at stores.”

Also Worth Reading

More Blog Posts in This Series

Breeding Freshness With Hydroponic Technology

The New Normal Will Be Anything But